Bank of Brodhead: A Core Deposit Success Story

5 min read

In an era where many community banks struggle to grow their stable funding base, The Bank of Brodhead stands out with a remarkable turnaround in core deposit growth.

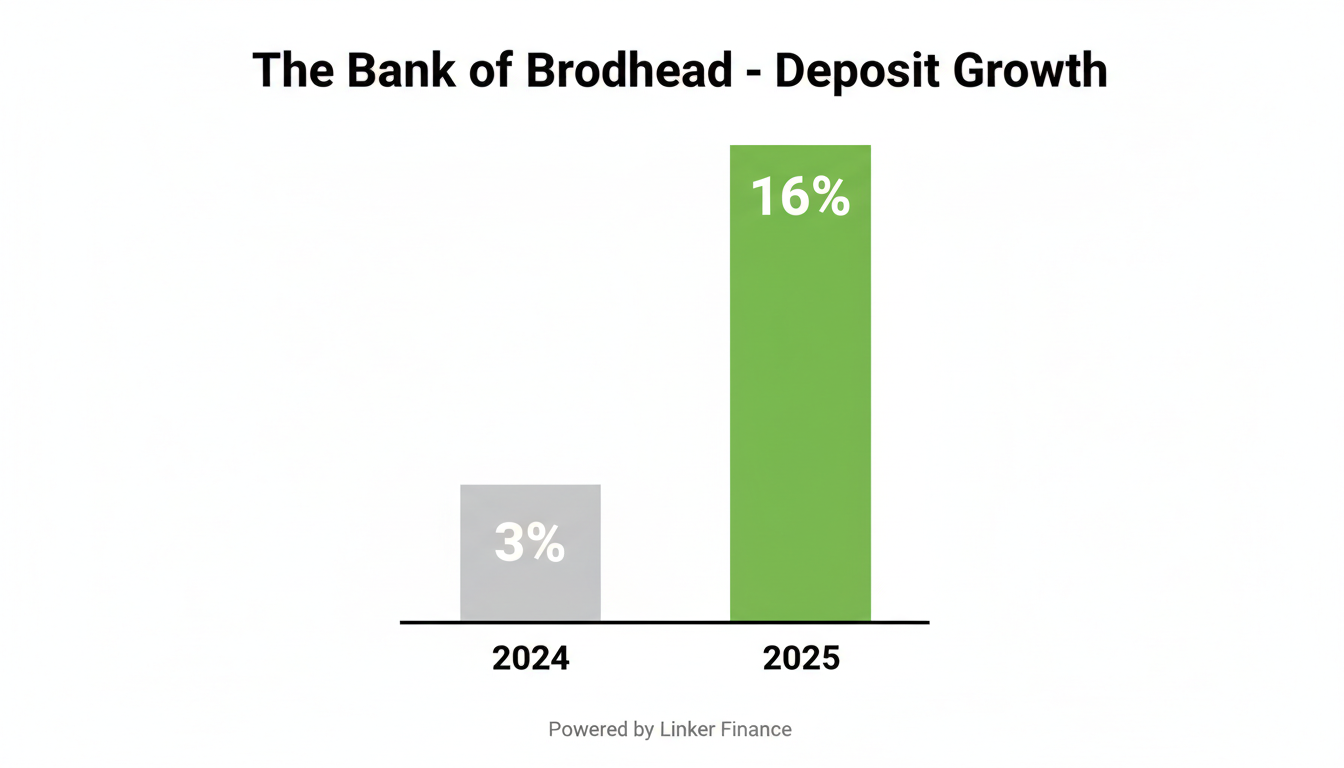

Core deposits at The Bank of Brodhead accelerated significantly — from just 3% growth in 2024 to 16% in 2025. This five-fold increase in growth rate signals a fundamental shift in the bank's deposit gathering capabilities.

Core deposits — checking accounts, savings accounts, and small CDs — represent the most stable and cost-effective source of funding for community banks. Unlike brokered or wholesale deposits that can quickly flee during market stress, core deposits tend to stay put.

For Bank of Brodhead, this acceleration in core deposit growth means:

Total deposits also grew impressively, rising 20.3% in 2025 compared to 9.7% in 2024. The bank's total deposits reached $328.6 million by the end of 2025, up from $273.1 million a year earlier.

More importantly, the gap between total deposit growth and core deposit growth is narrowing — a healthy sign that the bank is building a more sustainable funding base rather than relying heavily on rate-sensitive non-core funding.

The Bank of Brodhead's performance demonstrates that community banks can successfully grow their core deposit base even in a competitive rate environment. Their 16% core deposit growth in 2025 serves as a benchmark for other institutions looking to strengthen their funding mix.